National Bank Financial - Wealth Management (NBFWM) is a division of National Bank Financial Inc. (NBF), as well as a trademark owned by National Bank of Canada (NBC) that is used under license by NBF. NBF is a member of the Canadian Investment Regulatory Organization (CIRO) and the Canadian Investor Protection Fund (CIPF), and is a wholly owned subsidiary of NBC, a public company listed on the Toronto Stock Exchange (TSX: NA). The information contained herein has been prepared by Eric Van Enk, Associate Portfolio Manager and Wealth Advisor at NBF. I have prepared this article to the best of my judgment and professional experience to give you my thoughts on various financial aspects and considerations. The opinions expressed herein, which represent my informed opinions rather than research analyses, may not reflect the views of NBF. The opinions expressed are based on my analysis and interpretation of historical data. Values and returns will fluctuate, and past performance is not necessarily a guarantee of future performance. The particulars contained herein were obtained from sources I believe to be reliable but are not guaranteed by me and may be incomplete. The opinions expressed are based upon my analysis and interpretation of these particulars and are not to be construed as a solicitation or offer to buy or sell the securities mentioned herein. The securities or sectors mentioned herein are not suitable for all types of investors. Please consult your wealth advisor to verify whether the securities or sectors suit your investor's profile as well as to obtain complete information, including the main risk factors, regarding those securities or sectors.

Delayed Impact of Hikes

October 28, 2023 Insight from Eric Van Enk, Wealth Advisor Portfolio Manager

Delayed Impact of Hikes.

Has the full impact of higher interest rates been felt?

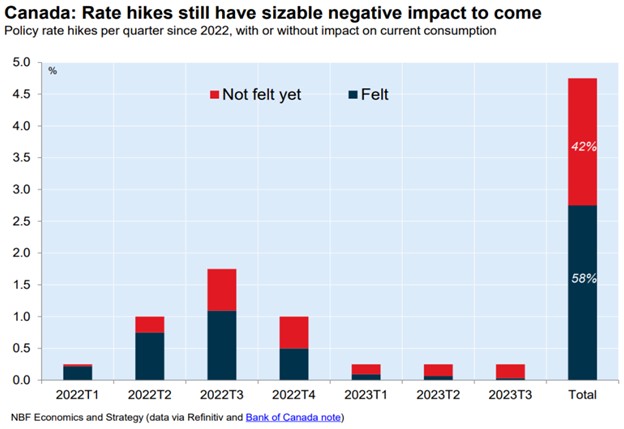

This week’s chart highlights the delayed impact of higher interest rates on the economy. The dark blue portion of the bar graph represents the impact of interest rate increases which have been felt by the economy. The red portion represents the impact which has not yet been felt by the economy. An increase in interest rates has a delayed impact on the economy for several reasons: some debt has a fixed interest rate which re-sets over time, consumers tend to draw-down savings before they reduce spending when the cost of debt increases, initial cost of borrowing increases are passed on to consumers through higher prices whereas later increases begin to reduce demand, etc.

Source: National Bank Financial

You can overlay this logic with your personal experience. When the

Bank of Canada increased interest rates in March of 2022, it likely

didn’t have an immediate impact on your life or spending habits.

However, now that we’re ~19 months into this rate hiking cycle, you

have likely experienced the impact of higher rates through higher

mortgage payments, higher rent, consumers spending less at your

business, etc. As you would expect, the chart shows that the first

increases made in the spring of 2022 have been almost fully reflected

in the economy. Conversely, the rate increases made this year have yet

to be meaningfully reflected in the economy. As shown in the chart,

the National Bank Financial Economics and Strategy team estimates that

42% of the impact of interest rate increases have yet to be felt. The

most recent Canadian economic data confirms that our economy has begun

to slow due to the cumulative impact of interest rate increases.

Canada’s most recent inflation data (CPI) showed a decrease of 0.1%

relative to expectations of an increase of 0.1% for the month of

September. The Bank of Canada’s preferred measures of inflation

(CPI-trim & CPI-median) also came in below expectations in

September. Furthermore, the most recent retail sales data declined by

0.1% for the month of August. This headline decline of 0.1% doesn’t

tell the entire story given Canada’s historic increase in immigration

levels. On a per capita basis, retail sales fell much further. When

our economics team annualizes August’s retail sales data and adjusts

for population growth, we estimate retail sales declined by 5.7% in

the third quarter which would be the worst quarterly performance since

the first pandemic lockdown.

If the economy has begun to slow and over 40% of the impact of higher interest rates has yet to be felt, it is very likely that the economy will continue to slow into 2024. The million-dollar question is, will inflation get back to the Bank of Canada’s 2% target, allowing them to reduce interest rates, before we experience a more substantial decline in economic activity. To quote the Governor of the Bank of Canada, Tiff Macklem, “the path to a soft landing has become very narrow”.